“Teachers Open The Doors, But You Must Enter By Yourself.” – Chinese Proverb

After the S&P 500 posted its best summer since 2009, the market took on a different tone as September started to unfold. A three-day pullback taking the S&P down about 7% while the NASDAQ lost 10% had a majority of analysts and investors concerned and downright nervous. For some apparent reason, the notion that pullbacks, corrections are part of the investing landscape of the equity market was once again forgotten. The slightest hint of stocks actually declining brings out the worst in the investment community. Common sense is tossed aside and emotion becomes the dominant force.

It appears there are three issues that are paramount in the mind of investors now. Market valuations, vaccines, and the election. Whenever the discussion rolls around to valuation, the next word is technology.

Heading into this pullback, the Technology sector was the market’s “gem” as it outpaced the S&P 500 by 28%. But just as Tech led the rally, it also declined the most in the latest round of selling. A common-sense approach understands how the markets work, the emotional approach incites the analysts to dust off the “Tech Wreck” articles. The speed and magnitude of the decline had investors questioning if history would repeat itself. In their minds, this was the 2000 Dot Com bubble bursting all over again.

No, it isn’t. There are several factors that differentiate the current state of the Tech sector from the Dot Com Era. Sure valuations for the Tech sector are elevated from a historical perspective, but they are well below the 2000 peak of 57x. I’ll argue they are justifiable given the earnings outlook. The sector is expected to show growth in earnings for 2020 and 2021 at 5% and 14% respectively; I believe those estimates are low.

At some point, the naysayers may come to realize what has been the message here since interest rates dropped off the cliff. Toss the historical norms out the window. Astute analysts have been telling investors interest rates should also be supportive, given that today’s 10-year Treasury yield of 0.68% is well below the 6.4% yield in 2000.

Today’s leading tech firms have stronger fundamentals and multiple revenue streams (hardware, software, services, cloud, content, etc.) rather than being one-trick ponies focused on a single product or service. Furthermore, the leaders continue to find new applications for existing technologies and invest in future technologies to remain competitive.

I expect many to now jump to the conclusion that there is a subliminal message telling investors to be “all-in” on the growth trade. Quite the contrary. The message for over four months, the “actionable advice”, spoke about the new economy macro trend that revolved around technology, and how it was the place to put money to work. While the rally was being questioned week after week that positioning worked out very well.

When an investor marries the fundamental picture with the technical view, it’s easy to then identify when “change” is in the air. Leaving out the latter leaves an investor on the side of the road with no food or water. That results in financial death. Trees don’t grow to the sky and after huge runs, many tech stocks will now enter a period of consolidation. That’s a function of what the price action is telling us, and it is displayed clearly in the “charts”. Rely strictly on hard data that is in the “present” and you lessen your chance of success.

Once this change was uncovered, I’ve been slowly playing the “reopening trade”. The new economy “Zoom” trade is not over, far from it. Logical assessment of that situation sees a period of sideways consolidation and perhaps a lean to the downside in “select names”. Once again it is going to come down to the other “actionable advice” presented here week after week, stock selection.

The same holds true when looking at the “old economy” companies. Not all “reopen” stocks are equal. Many industries will still lag and lag for a longer time than others. An investor has to be on the top of their game to be successful. They also need to use ALL of the tools available.

On the second concern regarding a vaccine for COVID-19, I have said repeatedly I wasn’t buying equities and keeping my equity allocation elevated because I was “playing” for a vaccine. I’ll repeat that I’m not a seller now because a vaccine may not be here tomorrow or this year.

The election should concern some investors. I say “some” because there are investors that fit into a category where this election is a mere “blip” in their investment life. So I’m not here to advise that ALL need to be ultra-cautious, raise a lot of cash, and get ready for volatility. That is simply a decision each investor has to make for themselves.

To that end, the consensus among analysts states that rallies are “selling events”. That coincides with the 11 headline articles that were highlighted last week warning investors about a severe market decline.

After posting losses for two consecutive weeks, buyers returned in a big way on Monday. It was a positive session with the S&P (SPY) rising 1.2%, and all other major indices joining in the rally. The Russell Small Caps (IWM) led all indices with a 2.7% gain and the Nasdaq (QQQ) wasn’t far behind rising 1.8%.

At the sector level Biotech (IBB) was up 5%, Autos (CARZ), Retail (XRT), Real Estate (XLRE), and Tech (XLK) all rose 2+%. All 11 sectors were positive, yes, even the Energy sector (XLE) posted a 0.76% gain. Breadth was 9:1 positive on the S&P 500.

There was no “Turnaround Tuesday” this week as buyers remained in control for another day. The Nasdaq Composite led the way gaining 1.2%, the S&P rose 0.50%, and the Dow 30 and Russell 200 were flat. I would classify market breadth as “neutral” today. With a close at 11,476 up 0.80% for the day, the Dow Transports is at a new recovery high and went totally unnoticed by many analysts. WTI rallied over 3%, the dollar was flat, and long-term interest rates pushed a touch higher in the wake of the 20-year bond auction.

The S&P was looking to make it four positive days in a row, but that wasn’t in the cards on Wednesday. The index closed at 3,385, down 0.4% on the day. The Dow 30 was flat, and Dow Transports rose 0.6%, while the Nasdaq was the big loser off 1.2%. Some of that money rolled into the Russell 2000 (small caps) which was the leader during the session rising 0.9%. In my view, the “rotation trade” controls the scene. Energy stocks surged 4% on the day as WTI gained just shy of 5% for its best day since June.

Selling pressure continued with downside probing to end the trading week. Plenty of “noise” and concern over the intraday moves, with a host of analysts calling for hedging strategies kept investors on edge. However, the “Weekly” tally doesn’t indicate everyone “ran for the hills”. The S&P was down 0.6%, the Nasdaq Composite lost 0.5%, and the Dow 30 was flat. In what is considered a healthy rotation, not all equities were sold. The Dow Transports closed with a gain of 1.5%, and the Russell Small caps rose 3%.

Relax, this is not unusual in a secular Bull market. In fact, it is very “healthy”.

Economy

The U.S. Census updated its Annual Social and Economic Supplement for 2019. This annual report contains detailed data on economic well-being, but unfortunately is quite lagged, coming out nine months into the year.

Bespoke Investment Group:

“This year the data is especially dated because it doesn’t contain any of the impacts of COVID, which has been the dominating driver of the economy for the last six months and will be for the foreseeable future.

Despite that, the ASEC still has a critical role to play in establishing the status of the economy over time, and this year does not disappoint in that respect. Starting with income, 2019 saw an impressive 6.8% median income growth for the median household in real terms.

Growth was strongest for Asian, African American, Hispanic, family or male-headed, foreign-born, and suburban households. Looking at the change in income over time, the last 8 years have seen very strong and sustained growth in real terms, including record gains in 2019 for median income.

Unlike the immediate post-financial crisis period, the last several years have seen sustained gains for the entire income spectrum, not just those with the highest income. As a result, income inequality has either stopped rising or is at least rising slower, depending on how you measure it.

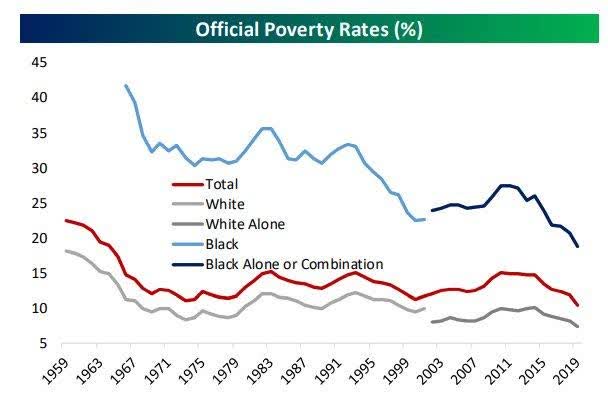

With stronger and more broadly shared income gains over the last few years, poverty has also been dropping steadily. 2019 saw record-low poverty rates by the official definition, and that drop is widely shared across demographics. As shown at left, the African American poverty rate is now below 20% for the first time on record; that is still nearly twice the total poverty rate and 2.5x as high as for Americans who are white alone, but the improvement over the last several years is at the very least dramatic by any standard. Poverty rates fell across every demographic group in 2019, with the biggest drops coming for African American and Asian Americans.”

Source; Bespoke

This data is important as it reinforces the Federal Reserve’s decision to stay with an accommodative policy. Strong growth of real incomes and large declines in poverty to record lows are the sorts of outcomes that a textbook would predict based on a central bank easing policy amidst below-potential economic growth. This data will help reinforce to the FOMC that it has room to continue running looser policy and returning the post-COVID economy to the gains we have seen to date.

The 0.4% U.S. industrial production gain in August left a fourth consecutive rise, with a weaker August increase than expected, but after big upward revisions that left August index levels just modestly short of our assumptions. The August headline gain reflected a 1.0% manufacturing rise that fell short of our estimate, with a surprising -5.7% drop in the vehicle assembly rate, alongside August drops of -2.5% for mining and -0.4% for utilities. The four-month industrial production climb has reversed 57% of the record two-month drop through March and April.

Empire State index surged 13.3 points to 17.0 in September after dropping -13.5 points to 3.7 in August. The increase was much larger than expected. The index is at its best level in two years. Also, this is the third month in expansion after the four months in contraction from March through June that included the historic nadir of -78.2 in April. The employment component edged up to 2.6 from 2.4 and is up from the -55.3 in April. The workweek jumped to 6.7 from -6.8. New orders firmed to 7.1 from -1.7. Prices paid climbed to 25.2 from 16.0, with prices received increasing to 6.5 from 4.7. The six-month outlook index was higher at 40.3 in September from 34.3 in August and hit its cycle low of 1.2 in March.

The Philly Fed drop to a still-solid 15.0 from 17.2 in August and 24.1 in July versus a 40-year low of -56.6 in April and a three-year high of 36.7 in February, left a fourth straight month of expansion. The component data were stronger than the headline, and the ISM-adjusted measure defied the headline down-tick with a 3.1 point pop to a seven-month high of 57.5 from 54.4 in August and 53.9 in July versus an all-time low of 29.8 in April and a five-month high of 58.3 in February. The Philly Fed headline drop, but with solid component readings, is in line with the Empire State bounce to 17.0 from 3.7 in August.

August retail sales increased by 0.6% and rose 0.7% excluding autos. Those are a little light of expectations and follow respective gains of 0.9% and 1.3%. Sales have been recovering from the pandemic plunge and have posted record gains of 18.3% and 12.3% in May after record lows of -14.7% and -15.2% in April. Strength in sales came from eating, drinking establishments which rose 4.7% from the prior 4.1% gain. Clothing sales climbed 2.9% from 2.2% previously and after more hefty gains in May and June. Furniture sales were up 2.1% from 0.9%, and building materials increased 2.0% from -2.4%. Auto and parts sales edged up 0.2% after July’s -1.0% drop. Gas station sales were up 0.4% versus 4.4%. Electronics sales rose 0.8% from 20.7% food/beverage sales dropped -1.2% from the prior 0.6%.

Another brick in the “economy is crumbling and we need more stimulus” wall was removed. Given the ball and chain that remains around the business community today, the consumer is hanging in there quite well.

The University of Michigan sentiment survey rose to a six-month high of 78.9 from 74.1 in August and 72.5 in July and left the measure above the 78.1 June prior pandemic-high. Current conditions rose to a three-month high of 87.5 from 82.9, while the expectations component rose to a six-month high of 73.3 from 68.5 in August and a seven-year low of 65.9 in July that was also seen in May.

This week’s release of the National Association of Homebuilders sentiment index for September surpassed all expectations. Economists were forecasting the headline index to come in at a level of 78, the actual reading was 83. Never before has the homebuilder sentiment index topped 80, let alone moved as high as 83.

Housing starts and permits were down month over month to multifamily but single-family continues to soar with single-family starts up 4.1% (12.1% y/y) and permits up 6% (15.6%). Overall starts are up 2.8% year over year and permits down 0.1%.

Global Economy

The OECD raised global GDP forecasts from -6% in 2020 to -4.5%, driven by smaller US and Eurozone recessions. 2021 growth has been cut from +5.2% to +5.0% and stated “economies will still need monetary and fiscal help for some time.”

Eurozone’s industrial production fell by 7.7 percent from a year earlier in July 2020, following a 12 percent slump in the previous month. Industrial production in aggregate and manufacturing specifically is still down about 7% from pre-COVID levels.

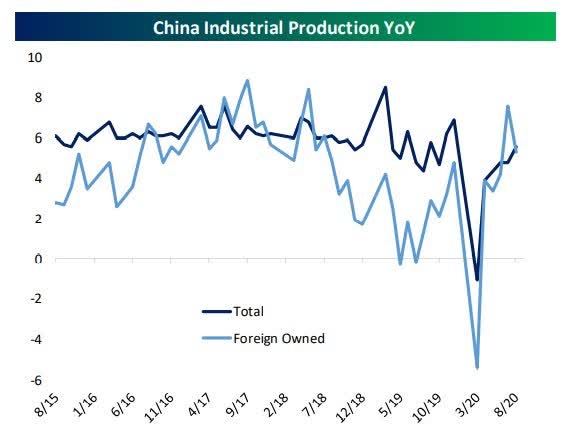

Chinese Industrial Production: If industrial production data is any indication, there is no “trade war”. As shown above, the growth of output from foreign-owned factories is now keeping pace with Chinese owned factories, reversing the 2018-2020 trend of slower output growth from foreign facilities that reflected supply chain adjustments amidst the US-China trade dispute.

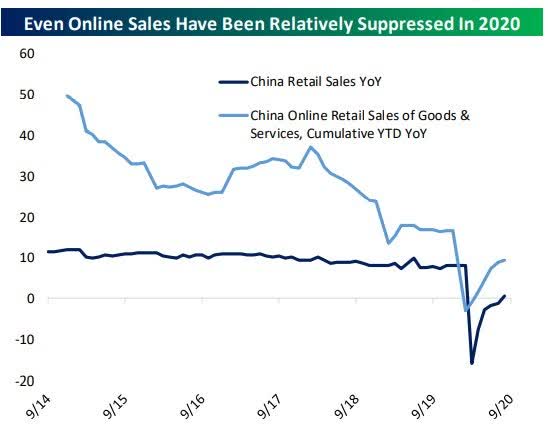

Chinese Consumption: Total retail spending by Chinese consumers is only barely positive year over year, and it’s not just a question of COVID either: even online sales, which should be relatively insulated, are growing much slower than pre-virus, a concern for the already investment-dependent Chinese economy.

The Political Scene

The Senate failed to advance a new fiscal relief bill proposed by Republicans as prospects for fiscal relief pre-election continue to decrease. However, the coming expiration of federal unemployment assistance, the potential need to provide supplementary FEMA funding, and the necessity for small business lending heading into the fall have the potential to boost negotiations in the near term.

On the election front, polls are showing the presidential race tightening in key swing states post-labor Day, as expected. However, Biden’s lead over Donald Trump is substantially higher in national polls compared to Hillary Clinton’s at this stage in the 2016 race. Biden is also performing significantly better than Clinton on candidate favorability, a factor that may maintain consistency in his support in the weeks ahead.

The Fed

The Federal Reserve FOMC policy statement:

“The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. With inflation running persistently below this longer-run goal, the Committee will aim to achieve inflation moderately above 2 percent for some time so that inflation averages 2 percent over time and longer-term inflation expectations remain well-anchored at 2 percent. The Committee expects to maintain an accommodative stance of monetary policy until these outcomes are achieved. The Committee decided to keep the target range for the federal funds rate at 0 to 1/4 percent and expects it will be appropriate to maintain this target range until labor market conditions have reached levels consistent with the Committee’s assessments of maximum employment and inflation has risen to 2 percent and is on track to moderately exceed 2 percent for some time. In addition, over the coming months, the Federal Reserve will increase its holdings of Treasury securities and agency mortgage-backed securities at least at the current pace to sustain smooth market functioning and help foster accommodative financial conditions, thereby supporting the flow of credit to households and businesses.”

Yield Curve

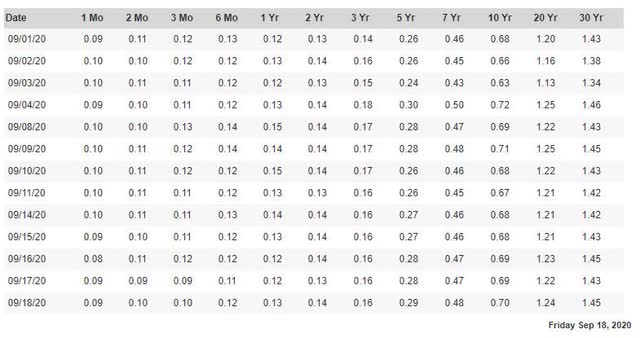

A trading range under 1% for the 10-year Treasury note has been in place for quite some time. After making a run to the top of that range in June, then testing the lows again, the 10-year bounced off the bottom and closed trading at 0.70%, rising 0.03% for the week.

The 3-month/10-year Treasury curve inverted on May 23rd, 2019, and remained inverted until mid-October. The renewed flight to safety inverted the 3-month/10-year yield curve once again on February 18th, 2020, and that inversion ended on March 3rd. The 2/10 Treasury curve is not inverted today.

Source: U.S. Dept. Of The Treasury

Source: U.S. Dept. Of The Treasury

The 2-10 spread was 30 basis points at the start of 2020; it stands at 56 basis points today.

Sentiment

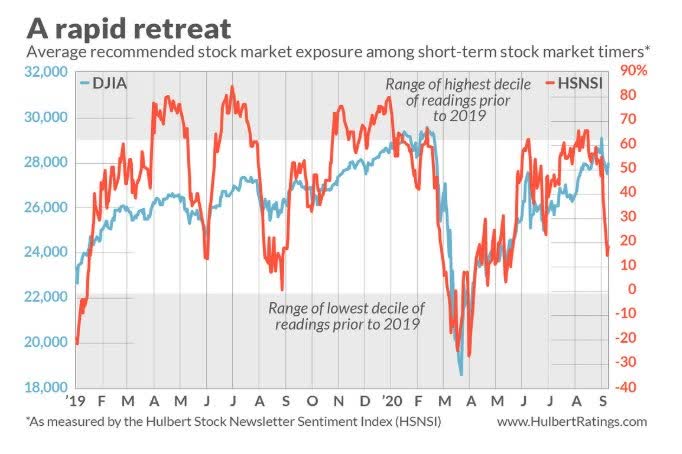

“Market timers” dropped equity exposure to 30%; Nasdaq exposure only 11%. “One of the most rapid retreats in more than 40 years”

Chart courtesy of Mark Hulbert

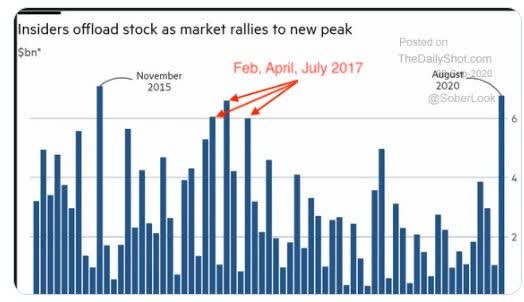

Want to follow the BEAR thesis that insider selling is a bad “omen”? Think again. Last month insiders sold the most stock since Nov 2015. Insiders sold heavily in 2017 and the S&P rose every month except one that year.

Chart courtesy of “TheDailyShot.com”

Bullish sentiment for individual investors saw an uptick over the last week, as this report had nowhere to go but up. According to the latest weekly survey from the American Association of Individual Investors, bullish sentiment increased from 23.7% last week to 32%.

The price of WTI rose above the resistance level of $42.50 for a couple of weeks, then turned around and tested the $35-$36 support level. The two-week slide in price ended when the price of crude closed at $40.88 on Friday which was a gain of $3.37 for the week. Energy stocks as measured by the Select Energy ETF (XLE) remain laggards but did post a gain of 3+% this week.

The Technical Picture

Investors saw plenty of downside probing last week before a key short-term support level was eventually violated.

Chart courtesy of FreeStockCharts.com

Chart courtesy of FreeStockCharts.com

The S&P closed the week below the 50-day moving average (blue line) for the first time since May. While the short-term trend is broken, the jury is out as to whether selling will continue to “test” the next support levels. Admittedly that view doesn’t align with the majority who now believe the index is about to fall off a cliff.

No need to guess what may occur; instead it will be important to concentrate on the short-term pivots that are meaningful. However, the Long-Term view, the view from 30,000 feet, is the only way to make successful decisions. These details are available in my daily updates to subscribers.

Short-term views are presented to give market participants a feel for the current situation. It should be noted that strategic investment decisions should NOT be based on any short-term view. These views contain a lot of noise and will lead an investor into whipsaw action that tends to detract from the overall performance.

Property and casualty insurers have come to find out the “reality” of this year’s round of “civil disorder” here in the U.S. Axios says 1 billion in property damage is the most expensive hit to the industry EVER.

Doubting there will be any quick change in how these “events” are handled, the insurance industry is rolling up its sleeves in anticipation of potential unrest following the November election, and getting ready to take another hit.

State Farm, Berkshire Hathaway (NYSE:BRK.A) (NYSE:BRK.B), Progressive (NYSE:PGR), Liberty Mutual Group, and Allstate (NYSE:ALL) are among the top five property and casualty insurers in the country.

Market Skeptics

Blackstone says we are setting up for a lost decade in stocks. It is nice to know I share the planet with people that can tell me what it will be like in 2027-2032. If that isn’t surprising enough, please consider that there will be a group of investors who actually believes this forecast will come to pass.

I remember being told the same thing in 2015 on the premise stocks had risen too much in a short period of time.

Individual Stocks and Sectors

Evidence that the “new economy” will continue to flourish:

“Amazon (AMZN) announced that it is hiring an additional 100,000 regular employment opportunities throughout the U.S. and Canada on top of the 33,000 corporate and technology jobs announced last week. The roles offer a starting wage of at least $15 per hour, and in select cities, Amazon is offering sign-on bonuses up to $1,000 to new hires. On top of Amazon’s minimum $15 wage, the company offers full-time employees benefits, which include health, vision, and dental insurance from day one, 401(K) with 50% company match, up to 20 weeks paid parental leave, and Amazon’s innovative career choice program, which pre-pays 95% of tuition for courses in high-demand fields.”

This also confirms that technology-based enterprises will help offset the employment issues with some of the “old economy” sectors that will continue to suffer (airlines, travel, lodging).

Big-cap stocks go higher and it’s a problem because it’s a “bubble”. Big-cap stocks pull back to remove the excess that has been created and it’s a problem because the market has lost its “leadership”. I didn’t agree with the first premise and I don’t agree with what is being said now about stocks like Amazon, Google (GOOG) (NASDAQ:GOOGL), Microsoft (MSFT), etc.

When these “new economy” stocks sell off, they are creating an opportunity. What investors are witnessing today is perfectly “normal”.

I like to use anecdotal evidence when investing. At the very start of trading this week, I listened to a conversation between a TV host and a respected financial analyst. The debate centered on the notion that Wall Street is still far removed from Main street. The host cited examples that in his “world,” no one is on the streets, store owners are shackled with guidelines that prohibit them from getting anywhere near “normal”.

I listened and then realized why this particular TV host was so passionate about his view that the economy was still horrible. He was speaking to his observations and experiences in New York and New Jersey. For those who haven’t been keeping score, those two states along with California continue the “ball and chain” approach that shackles the business world in their states. Of course, his opinion is then extrapolated to the equity markets and the conclusion was obvious. Wall Street can’t see the reality of “Main Street”, therefore, one simply can’t invest in this overhyped, overvalued market. That also happened to be his closing remarks.

Therein lies the danger of not looking around and seeing the “big picture”. I can assure you many investors took that view and are still taking that same approach today. They convinced themselves to get out and stay out of stocks, and pundits wrote article after article to convince the average investor to do the same. The well-informed cited the “big picture data” that looks at what is occurring around the country and the globe instead of regions that remain locked down.

In addition, there are many other signs to take note of. The macro change on display when the Q2 earnings season was in full swing in the “new economy” companies showed how their businesses trumped many of the roadblocks that are still in place. Trucking and rail companies along with package delivery stocks like FedEx (NYSE:FDX) and UPS (NYSE:UPS) are at all-time highs. The transportation index at a new recovery high with the airline industry a mere shadow of itself with a LONG road to recovery. That is sending a message that the economy is growing, not contracting.

The entire U.S. economy has never been locked down. No one here has ever seen the federal government spend $2.8 trillion to keep that economy afloat. A quick recession is over, stocks rebounded and the secular Bull market resumed in April of this year. Far too many underestimated the role technology plays in our lives today. The U.S. private economy transformed itself when the COVID lockdowns emerged into a “virtual” world in which an enormous amount of economic activity was conducted in ways we never dreamed of.

There will be many roadblocks to an eventual full recovery. The stock market has anticipated much of the recovery that has taken place. Investors can expect a bumpy ride from here, playing a guessing game on every 5-10% move is not part of my playbook. If you believe the technological advances have ended and the old economy won’t ever get back to anywhere near normal because of any number of “issues”, then sell your equity holdings. There are plenty of Savvy Investors that are looking for a “bargain”

Please allow me to take a moment and remind all of the readers of an important issue. I provide investment advice to clients and members of my marketplace service. Each week I strive to provide an investment backdrop that helps investors make their own decisions. In these types of forums, readers bring a host of situations and variables to the table when visiting these articles. Therefore it is impossible to pinpoint what may be right for each situation.

In different circumstances, I can determine each client’s personal situation/requirements and discuss issues with them when needed. That is impossible with readers of these articles. Therefore, I will attempt to be helpful in forming an opinion without crossing the line into specific advice. Please keep that in mind when forming your investment strategy.

to all of the readers that contribute to this forum to make these articles a better experience for everyone.

to all of the readers that contribute to this forum to make these articles a better experience for everyone.

Best of Luck to Everyone!

“Change” is in the air and in the charts of many companies that are tracked by the Savvy Investor Marketplace. Relying on ONE view and ONE tool brings a knife to a gunfight. That investor is left for dead in this fast-changing investing environment we find ourselves in today.

The Election, Valuation, Political gridlock, etc. are making investors very anxious these days. It’s time to STOP guessing, STOP making decisions based on a “feeling”.

Instead, take advantage of ALL of the research and years of experience that is at your disposal when you join the community of Savvy Investors.

We remain ONE STEP ahead.

Disclosure: I am/we are long EVERY STOCK/ETF IN THE SAVVY PLAYBOOK. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: My portfolios are ALL positioned to take advantage of the bull market with NO hedges in place.

This article contains my views of the equity market, it reflects the strategy and positioning that is comfortable for me.

IT IS NOT A BUY AND HOLD STRATEGY. Of course, it is not suited for everyone, as each individual situation is unique.

Hopefully, it sparks ideas, adds some common sense to the intricate investing process, and makes investors feel calmer, putting them in control.

The opinions rendered here, are just that – opinions – and along with positions can change at any time.

As always I encourage readers to use common sense when it comes to managing any ideas that I decide to share with the community. Nowhere is it implied that any stock should be bought and put away until you die.

Periodic reviews are mandatory to adjust to changes in the macro backdrop that will take place over time. The goal of this article is to help you with your thought process based on the lessons I have learned over the last 35+ years. Although it would be nice, we can’t expect to capture each and every short-term move.